SECURE 2.0 Changes Aimed at Savings Gap

After almost three years of proposals and discussions, SECURE 2.0 became law at the end of 2022. It builds on the retirement savings policy initiatives addressed in the SECURE Act of 2019, which are

intended to help workers achieve a financially secure retirement. SECURE 2.0 contains 92 provisions that change retirement plan and IRA rules in myriad ways to incentivize small employers to offer

retirement plans, simplify aspects of plan administration, help participants address emergency savings needs and student loan debt while saving for retirement, raise contribution limits, and ensure that more

workers have increased chances to enroll in a workplace retirement plan.

There is much to talk about with SECURE 2.0, though many of its provisions won’t take effect until 2024, 2025, or 2026. This gives service providers, document drafters, and plan sponsors time to ensure that the changes are incorporated in compliance with the new law while affording regulators time to issue guidance on administrative details. The Department of Labor, Treasury, and IRS are expected to produce SECURE 2.0 guidance sometime this year. For now, this newsletter will address some topics that will affect 401(k), 403(b), and governmental 457(b) plans in 2023, along with what plan sponsors should think about now to get ready for next year.

More Changes to RMDs—Starting Now

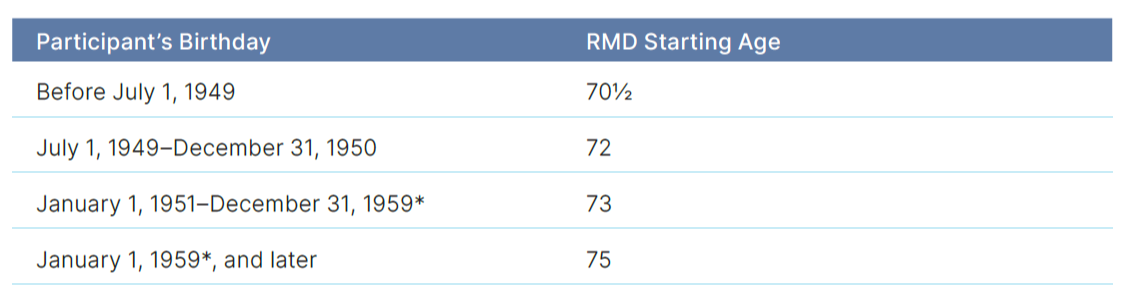

SECURE 2.0 increases the age at which plan participants (and IRA owners) must begin taking required minimum distributions (RMDs) from 72 to 73 for those who turn 72 after December 31, 2022. This change is effective for RMDs due for 2023 (not for RMDs due for 2022 but taken in 2023). SECURE 2.0 will raise the RMD starting age again, in 2033, to 75 for those who turn 74 after December 31, 2032. This change will allow participants who don’t need to dip into their plan accounts for retirement income to keep their savings invested and tax deferred for longer. The following table breaks down which participants are subject to which RMD age, based on birthdate.

* SECURE 2.0 contains what is believed to be a typographical error, resulting in those born in 1959 being subject to both the age 73

and age 75 requirement. This is expected to be corrected or clarified well before 2033.

Plan participants and IRA owners also receive a tax break if they fail to withdraw their RMD in a timely manner. Effective for 2023, the participant’s excise tax for failing to withdraw an RMD when required is

reduced from 50 percent to 25 percent of the amount not taken. The tax will be further reduced to 10 percent if the RMD is taken within a two-year correction window.

More good news for retirement savers who are trying to build tax-free wealth for retirement or their heirs takes effect in 2024, when designated Roth accounts in workplace retirement plans will no longer

be subject to RMDs while the account owner is alive. This means a plan participant’s Roth account balance should be excluded when calculating their RMD each year. Excluding designated Roth accounts

from RMDs matches the treatment for Roth IRAs and could reduce the amount of assets being rolled from retirement plan Roth accounts to Roth IRAs to escape RMDs.

SECURE 2.0 also made one more change to RMD/beneficiary distribution rules, which were significantly modified by the SECURE Act of 2019. This new change, effective in 2024, allows a spouse

beneficiary who is the sole beneficiary of a participant who died before beginning RMDs to elect to have beneficiary payments calculated using the spouse’s age and the Uniform Lifetime Table, as if the

spouse were the plan participant, rather than using the beneficiary Single Life Table. This should result in smaller required annual payments. Outstanding questions remain regarding the election and how this change affects beneficiary payment options when the participant’s death occurs after starting RMDs.

The Treasury and IRS are working on RMD regulations to implement the beneficiary rule changes made by the SECURE Act of 2019. Because those regulations aren’t finalized, they may include details on this SECURE 2.0 change when they are released.

Plan sponsors will want to work with their recordkeepers to make the operational changes necessary to implement the new RMD starting age of 73 this year, along with ensuring that processes are in place to exclude Roth accounts from RMD calculations next year. Watch later this year for information on Treasury regulations that should bring more clarity to all beneficiary rule changes.

Roth Accounts on the Rise

Congress has been focusing on Roth accounts in retirement plan-related legislation over the past several years. This is partly because Roth contributions are made on an after-tax basis, so they don’t

“cost” the federal government tax revenue in the way that provisions providing an upfront tax break do (e.g., pretax deferrals reduce taxable income). Roth contributions, therefore, become revenue raisers

for Congress when making tax law changes. SECURE 2.0 is no exception; it contains several provisions that push more contributions into a Roth account.

Here are a few:

1. Optional: Beginning in 2023, plan sponsors may choose to allow participants to designate employer contributions made on their behalf as Roth contributions. These contributions must be vested when

made and will be included in the participant’s taxable income for the year. (Although this is effective for 2023, more guidance is needed on participant elections, along with tax withholding, reporting, and timing requirements.)

2. Optional: Beginning in 2024, plan sponsors may add emergency savings accounts (ESAs) to their plan to help participants save for financial emergencies and retirement. ESA account balances are

capped at $2,500 (plus investment earnings) and must be Roth accounts. Distributions must be allowed monthly and won’t be taxable to the participant because the Roth contributions have

already been taxed. When participants terminate from service with a balance in an ESA, the plan must allow the participant to transfer the balance to another Roth account in the plan.

3. Mandatory: Beginning in 2024, if a retirement plan allows participants ages 50 and older to make catch-up contributions, those contributions must be made to a Roth account if the participant’s

prior-year compensation from the sponsoring employer exceeds $145,000.

Although many SECURE 2.0 changes are optional for plan sponsors to adopt, some are mandatory—which means plan sponsors who don’t already offer designated Roth contributions

in their plan may want to explore the process and costs of adding them to their plans now to avoid future operational issues.

Catch-Up Contributions in Jeopardy?

In addition to mandating that high-earning participants making catch-up contributions make them on an after-tax basis to a Roth account, SECURE 2.0 increases the amount of catch-up contributions that certain participants may make to a workplace retirement plan. Beginning in 2025, plan participants ages 60, 61, 62, and 63 may make catch-up contributions for one year up to the greater of $10,000 or an amount equal to 150 percent of the regular catch-up contribution limit in effect for 2024. (The catch-up contribution limit for 2023 is $7,500 and may be indexed in future years.)

The provision to increase the catch-up contribution limit was included in both House and Senate proposals with different details that had to be reconciled to make it into the final bill. It’s clear Congress

settled on the increase noted here, as well as the Roth mandate for high earners only (versus all catch-up contributors). As Congress drafted the legislative text, however, it eliminated the text that allows catch-up contributions. As written, no retirement plan catch-up contributions will be allowed after 2023. This error needs to be addressed by technical correction legislation or an IRS pronouncement, which is expected to happen by next year.

Catch-up contributions are subject to complex changes. In addition to tracking who is eligible to make a catch-up contribution because they are 50 or older and have exceeded a plan,

salary deferral, or testing limit, plan sponsors must track who is 60–63 and eligible to make the increased contribution amount each year, as well as keep track of which catch-up

contributors earned more than $145,000 in the previous year to ensure that their catch-ups are made as Roth contributions. Plan sponsors may simply choose not to offer catch-up

contributions in future plan years to avoid the administrative complexity. Or they may develop a process (in conjunction with recordkeepers) with the necessary data points to track

catch-up eligible participants and contributions to ensure compliance with the new rules.

We Can Help

We are ready to provide you with the ideas, guidance, and foresight to position your firm for success. If you would like to review your plan’s features, operations, or industry developments that may affect your plan, we’re here to assist you.

Commonwealth Financial Network® does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation. Securities and advisory services offered through Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services are separate from and not offered through Commonwealth Financial Network.